By working with industry experts from leading companies such as Chevron, Google, Microsoft, Merck and McKinsey, as well as partnering with universities such as Stanford and Texas A&M, the Institute is working to improve the value that engineering and construction provide to the economy and to society. Join PPI to make Project Production Management the dominant solution for successful project delivery.

Over $1.6 trillion is wasted annually due to capital projects not being delivered on time or on budget. [1] A staggering 98% of projects over $1 billion are failing to meet their original objectives [2], despite enormous investments in stage gate processes, benchmarking, collaborative forms of contracts, software and other improvement efforts. This massive amount of waste has profound implications for world economies and for society as a whole. As chronic cost overruns and delays continue to destroy value, this loss not only translates to increased project costs, but also impacts daily life due to delayed output of clean water, affordable energy, dependable communication, safe and efficient structures and reliable transportation.

This matters because the engineering and construction industry comprises one eighth of the world’s total economic output [2]. No other industry can survive without some form of construction. The industry’s combination of size and inefficiency is staggering, resulting in a significant opportunity to capture lost value. Even a 1% efficiency improvement creates value of over $150 billion annually.

It is evident that the engineering and construction industry applies sophisticated scientific analysis to the design of the asset. For example, buildings that can survive earthquakes, bridges that span amazing distances and heights, colossal dams providing electricity and stadiums that can host tens of thousands of people under one roof. These are all examples of the application of many branches of science and engineering to ensure the end product functions as it is designed. Unfortunately, this same approach has not been successfully applied to the actual delivery of the projects themselves.

To this extent, it is important to understand that project delivery has developed over three distinct eras [3]:

Era 1 – Productivity

Era 2 – Predictability

Era 3 – Profitability

In the late 1800’s and early 1900’s Frederick Taylor, a mechanical engineer, began development of Scientific Management. Having observed the need to enhance productivity in the works or shop, Taylor believed workers had a disposition to not work productively and set out to develop an approach to address this problem. [4] The Era 1 focus was on productivity of workers and work in traditional manufacturing by separating planning from doing and by establishing the most efficient standards for work. Daniel Hauer followed Taylor and applied Scientific Management to construction. Hauer’s Era 1 approach was incomplete as evidenced by continued problems with project delivery and subsequent attempts to bridge the gap. Meanwhile, manufacturing began a steady productivity improvement journey.

In the 1950’s, Era 2 project delivery efforts emerged with the advent of computer technology as applied to projects. The primary characteristic of Era 2 efforts was a focus on predictability of capital project delivery. Approaches such as Critical Path Management (CRM), Performance Evaluation and Review Technique (PERT) were developed and, later, techniques such as Earned Value Management (EVM), the Phase-Gate Process, Advanced Work Packaging (AWP) and Work Face Planning (WFP). Today, these approaches are all recognized as part of Project Management, a defined profession with its own body of knowledge, the Project Management Body of Knowledge (PMBOK).

The Project Management Institute (PMI) publishes PMBOK and includes knowledge areas such as project scope, time and cost management, quality, risk and procurement management. Though these functions are essential to managing projects, they are by no means the only activities required to support successful project outcomes.

The conventional approach is missing a crucial insight – understanding that projects are production systems, and as such, should be managed using the concepts of Operations Management and its foundation on Operations Science. This project delivery omission of Operations Science and Operations Management is exemplified in PMI’s PMBOK:

“Operations management is a subject that is outside the scope of formal project management as described in this standard.

Operations management is an area of management concerned with the ongoing production of goods and/or services. It involves ensuring that business operations continue efficiently by using the optimum resources needed and meeting customer demands. It is concerned with managing processes that transform inputs (e.g. materials, components, energy and labor) into outputs (e.g. products, goods, and/or services)” [5].

The behavior encouraged here is to ignore Operations Management as part of Project Management, so its practices and science are not a part of actual project delivery methods. Many are of the opinion that Operations Management only applies to post-project delivery phases.

During Era 2, construction companies that operated under direct hire business models looked for ways to minimize risk, and therefore, shifted to Construction Management (CM), wherein they became agents of the owner. New forms of commercial models, including the guaranteed maximum price (GMP) model, became prevalent under this approach. CM and GMP changed contractors from construction companies to management companies, and in so doing, their area of expertise moved from designing, making and building to more administrative activities required to manage contracts and others performing the actual work.

In summary, immense efforts have been made to improve productivity and predictability of capital projects with consistently poor results. One common characteristic among all these approaches is a gap in understanding project performance as a function of production system performance – not project controls. Project Production Management (PPM) uses a scientific approach to production system performance to close this gap and implement the productivity improvements long pursued by the engineering and construction industry.

Unlike Eras 1 and 2, Era 3 focuses on how best to achieve profitability. In the early to mid 1990’s, a group of people affiliated with Stanford University and the University of California at Berkeley (UCB) began to question engineering and construction industry practices and started the development of a new construct for the delivery of capital projects. These efforts considered different production system models used in the automotive industry documented by the book, The Machine that Changed the World, [6] followed by deep interest in how Operations Science, as described in Factory Physics, [7] could be applied to optimize the delivery of capital projects. This was the beginning of Era 3 in project delivery.

Through these efforts, what became apparent was the complete lack of scientific understanding of production by those managing capital projects. Project Controls professionals were observed creating schedules for purposes of invoicing, measuring progress and potential claims with little, if any, relation to the actual work and its true complexity being performed in engineering, fabrication and site construction. What was missing was a comprehensive approach for understanding and managing both craft and knowledge work as production systems.

Though it garnered little attention at the time, a fundamental insight to project structure is provided in the Product / Process Matrix created by Hayes and Wheelwright. In 1986, Roger Schmenner (see figure below) added projects to the matrix as a formal type of production system.

While Schmenner’s version of the Product / Process matrix shows a project as single type of process, or production system, a wider view reveals that projects, including their supply networks, are collections of all of the production systems shown in the matrix.

In the study of production systems, there exists two key elements: demand and supply. Demand is what the customer seeks, and supply is what the product supplier or service provider delivers. In the world of project management, there is an over emphasis on demand with little, if any attention paid to the production systems that make supply possible. During the past fifty years, the project focus has largely been on the demand side, i.e., what needs to be done, by who and when. This is managed through scope, contracts and dates. An Era 2 Critical Path Method schedule, or any schedule for that matter, is merely a representation of potential demand.

Supply is comprised of the network of processes, operations and resources that comes together through various organizations to make and deliver to demand. Due to the gap in Eras 1 & 2 project management understanding, project professionals know little about how a project’s supply side production systems operate and much less about the basic science required to manage those production systems to achieve best possible project performance.

When viewed through an Operations Science lens, the deficiencies in current project delivery approaches become evident.

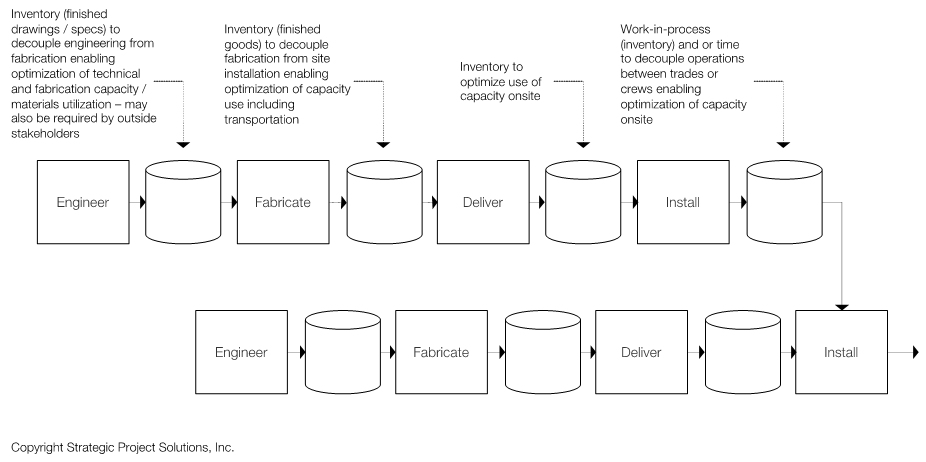

For example, Operations Science establishes that inventory is a proxy for time. As with any production system, understanding and managing inventory (see below) is a critical element of success, yet Era 1 and Era 2 constructs ignore inventory. As a result, project sites are often flooded with stocks of materials and immense volumes of work-in-process. Project managers see the piles and warehouses of excess inventory (stock and WIP) as a panacea rather than as a potential detriment causing project delays and cost overruns.

For knowledge workers, e.g. design engineers, the same holds except the inventory is not physical WIP, it’s virtual WIP such as simulations required or drawing checks or tests completed. Knowledge work is usually some sort of task that requires resource, an engineer or project manager, capacity. The typical goal in knowledge work is to keep the production resources, knowledge workers, busy.

Scope, schedule dates and cost estimates are absolutely required for projects, but the project’s production systems will dictate project results. Understanding and influencing project production systems through Project Production Management is crucial to realizing project objectives.

Traditional project management is primarily based on the functional activities associated with delivering a project, i.e., what (scope and quality), done when (schedule) by whom (resource). See top row in figure below. This typical project management view is reflected in the “iron triangle” construct, take any two but the third has to change. Design something quickly to a high standard, it will not be cheap. Design something quickly and cheaply, it will not be of high quality. Design something of high quality with low cost, it will take a long time.

Project Production Management (PPM) provides the means to map, model, analyze, simulate, optimize, control and improve project production systems. The scope and schedule for a project determine what should be done. Appropriate control of a project’s production systems determine what will be done and how well project outcomes will be achieved. See bottom row in figure above. The application of Operations Science theories, principles, methods and leading-edge technology to better understand, control and improve project delivery closes the gap that has caused chronic project delivery failure for over hundred years.

The Project Production Institute (PPI) exists to enhance the value Engineering and Construction provides to the economy and society. We are working to: 1) make PPM the dominant paradigm for the delivery of capital projects, 2) have project professionals use PPM principles, methods and tools in their everyday work, 3) create a thriving market for PPM services and tools, 4) fund and advance global PPM research, development and education (higher and trade), and 5) ensure PPM is acknowledged, required and specified as a standard by government and regulatory agencies.

To that end, the Institute partners with leading universities to conduct research and educate students and professionals, produces an annual Journal to disseminate knowledge, and hosts events and webinars around the world to discuss pertinent and timely topics related to PPM. In order to advance PPM through access and insight, the Institute’s Industry Council consists of experts and leaders from companies such as Chevron, Google, Microsoft and Merck.

Join us in eliminating chronic poor project delivery performance . Become a member. Attend an event. Participate in research. Stay informed. Learn more about how PPM is addressing this critical gap.

[1] F. Barbosa, J. Woetzel, J. Mischke and et al, “Reinventing Construction: A Route to Higher Productivity,” February 2017. [Online]. Available: https://mck.co/2FaftfB. [Accessed September 2020].

[2] S. Changali, A. Mohammad and M. van Nieuwland, “The construction productivity imperative,” 1 July 2015. [Online]. Available: https://www.mckinsey.com/industries/capital-projects-and-infrastructure/our-insights/the-construction-productivity-imperative. [Accessed September 2020].

[3] R. G. Shenoy and T. R. Zabelle, “New Era of Project Delviery – Project as Production System,” Journal of Project Production Management, vol. 1, no. 1, pp. 13-24, 2016.

[4] F. W. Taylor, The Principles of Scientific Management, New York: Harper & Bros., 1911.

[5] Project Management Institute, A Guide to the Project Management Body of Knowledge (PMBOK Guide), Newtown Square, Pennsylvania: Project Management Institute, 2017, p. Section 1.2.3.4 OPERATIONS MANAGEMENT.

[6] J. P. Womack, D. T. Jones and D. Roos, The Machine That Changed The World, New York: Free Press, 1990.

[7] W. Hopp and M. Spearman, Factory Physics, 3rd Edition, Long Grove, Illinois: Waveland Press, Inc., 2008.